05.22.23

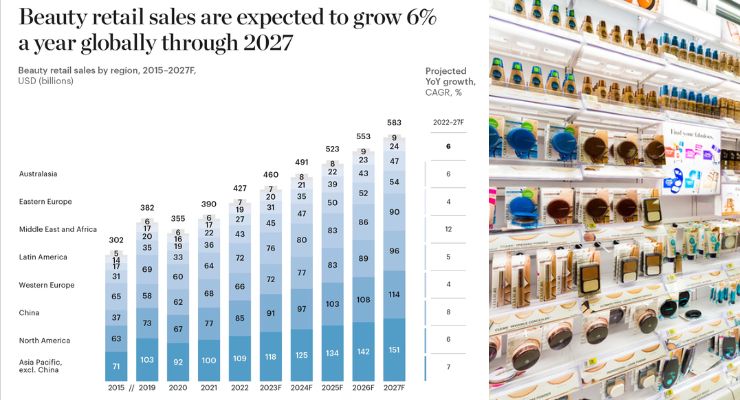

A new report from The Business of Fashion (BoF) and McKinsey and Company, reveals that the global beauty industry is in the midst of a new era of growth and expansion, with global retail sales expected to reach an estimated $580 billion by 2027.

The report also identifies several critical dynamics for the industry over a five-year period to 2027: geographic rebalancing; the need for indies to scale; merger and acquisition opportunities; Gen-Z’s influence; and wellness and self-care expansions.

“We are witnessing a change in how consumers think about beauty. It’s no longer solely about lipstick and skincare but a holistic approach to how these products make us feel about ourselves and the world around us,” said Priya Rao, Executive Editor at The Business of Beauty, The Business of Fashion. “Our report pairs in-depth research with our expert industry analysis to look ahead at what the market can expect over the next few years.”

In addition to exploring opportunities in both China and the U.S., the report zeros in on the Middle East and India as examples of markets that beauty players may consider. In the Middle East and Africa, beauty retail sales are forecasted to reach $47 billion by 2027, due in part to economic modernization under new government programs and relatively high household income, among other factors.

India, worth $14 billion, is expected to increase to $21 billion by 2027, spurred by burgeoning levels of disposable income and a large younger, digitally savvy generation of shoppers.

Today’s $1.5 trillion global wellness industry is projected to grow by up to 10% by 2027 and will be reflected in the rise of product offerings that merge beauty and wellness. McKinsey’s consumer survey found that wellness products expected to rise in popularity include: sleep (30% of respondents say they regularly use sleep-enhancing products and services), sexual wellness (with approximately 20% of consumers today using such products) and supplements (ranging from vitamins and adaptogens, to snacks and beverages infused with beauty and health-promoting benefits).

Similar to fashion purchases, beauty shoppers are also focused on sustainability. When asked about the top three aspects of sustainability that matter most when making beauty purchases, survey respondents cited: an absence of ingredients that harm the environment, 100% natural formulas, and cruelty-free production.

1. The New Growth Map: China and the US will continue to be major markets for beauty but other markets must also now be part of brands’ and retailers’ growth strategies.

2. Wellness Awakens: Consumers are shifting their understanding of beauty from purely aesthetics to encompass holistic wellbeing, creating new opportunities in subcategories such as sleep, sexual wellness and ingestible beauty supplements.

3. Decoding Gen-Z: Brands must adapt product portfolios, channel mixes and marketing strategies in order to resonate with the younger generation of shoppers who prioritize value and efficacy when selecting beauty products.

4. The Scale Imperative: For young brands scaling is becoming increasingly difficult in a very crowded market and to scale brands will need to focus on channel and geographic expansion.

5. M&A Recalibrated: In the short term, beauty mergers-and-acquisitions activity may not deliver as many megadeals as seen across the industry in the past, but the deal making will continue to be buoyant

“The State of Fashion: Beauty,” a new report from The Business of Fashion and McKinsey & Company, is released ahead of The Business of Beauty Global Forum 2023. Read the full report.

- Skincare, fragrance, color cosmetics and hair care all expected to grow globally between 2022 and 2027.

- Skincare, as beauty’s largest category, is expected to grow from $190 billion to $260 billion, driven by innovation and shoppers seeking out products focused on science-based efficacy.

- Fragrance retail sales are expected to rise from approximately $70 billion to nearly $100 billion, benefitting from further expected penetration in China and growth in the US.

- Color cosmetics is expected to continue its post-pandemic recovery, rising from $80 billion to around $105 billion, with growth largely evenly distributed across price segments.

- Hair care (excluding devices) is expected to expand from $90 billion to $120 billion, with the category experiencing a “skinification” as consumers adopt multi-step hair care routines much as they have been doing with skincare.

The report also identifies several critical dynamics for the industry over a five-year period to 2027: geographic rebalancing; the need for indies to scale; merger and acquisition opportunities; Gen-Z’s influence; and wellness and self-care expansions.

“We are witnessing a change in how consumers think about beauty. It’s no longer solely about lipstick and skincare but a holistic approach to how these products make us feel about ourselves and the world around us,” said Priya Rao, Executive Editor at The Business of Beauty, The Business of Fashion. “Our report pairs in-depth research with our expert industry analysis to look ahead at what the market can expect over the next few years.”

Shifting Geographic and Category Priorities

Beauty has cemented its reputation as a resilient industry that can consistently deliver high margins and new avenues of expansion. According to the report, this will continue but will require beauty players to deepen their geographic diversification: while the U.S. and China are expected to remain the industry’s heavyweight markets, others could play larger roles in driving revenues than they have in the past.In addition to exploring opportunities in both China and the U.S., the report zeros in on the Middle East and India as examples of markets that beauty players may consider. In the Middle East and Africa, beauty retail sales are forecasted to reach $47 billion by 2027, due in part to economic modernization under new government programs and relatively high household income, among other factors.

India, worth $14 billion, is expected to increase to $21 billion by 2027, spurred by burgeoning levels of disposable income and a large younger, digitally savvy generation of shoppers.

The Rise of Wellness

Since the late 2000s, wellness and self-care have assimilated into the mainstream and today consumers are seeking out products that support their aesthetic needs as well as physical and mental health. The majority of consumers from the U.S., China and Europe said they plan to increase spending on wellness products and services in the year ahead.Today’s $1.5 trillion global wellness industry is projected to grow by up to 10% by 2027 and will be reflected in the rise of product offerings that merge beauty and wellness. McKinsey’s consumer survey found that wellness products expected to rise in popularity include: sleep (30% of respondents say they regularly use sleep-enhancing products and services), sexual wellness (with approximately 20% of consumers today using such products) and supplements (ranging from vitamins and adaptogens, to snacks and beverages infused with beauty and health-promoting benefits).

Buying into Beauty: Consumer Behavior

To enrich this report’s industry analysis and explore beauty shoppers’ preferences, McKinsey conducted a consumer survey in six major markets — China, the U.S., the UK, France, Germany and Italy. Among other findings, 40% of consumers indicated they are loyal to the brands they know and trust, while a greater proportion—69%—said they like to try new products at least every six months. The survey also surfaced insight into shopping journeys, where consumers cited in-store as their preferred method of shopping (45%), followed by online (40%).Similar to fashion purchases, beauty shoppers are also focused on sustainability. When asked about the top three aspects of sustainability that matter most when making beauty purchases, survey respondents cited: an absence of ingredients that harm the environment, 100% natural formulas, and cruelty-free production.

Key Takeaways

Five themes cut across all four beauty categories to reshape the beauty industry:1. The New Growth Map: China and the US will continue to be major markets for beauty but other markets must also now be part of brands’ and retailers’ growth strategies.

- And the Middle East are emerging as growth hotspots, with retail sales expected to increase to $21 billion in India and $47 billion in the Middle East and Africa by 2027.

2. Wellness Awakens: Consumers are shifting their understanding of beauty from purely aesthetics to encompass holistic wellbeing, creating new opportunities in subcategories such as sleep, sexual wellness and ingestible beauty supplements.

- Today’s $1.5 trillion global wellness industry is projected to expand retail sales at a 10% CAGR between 2022 and 2027.

3. Decoding Gen-Z: Brands must adapt product portfolios, channel mixes and marketing strategies in order to resonate with the younger generation of shoppers who prioritize value and efficacy when selecting beauty products.

- Gen-Z is more loyal than many brands may think. Even as they desire to try new products, nearly 60 percent are willing to keep buying from their favorite brands.

4. The Scale Imperative: For young brands scaling is becoming increasingly difficult in a very crowded market and to scale brands will need to focus on channel and geographic expansion.

- Of a group of 46 brands with global retail sales between $50 million and $200 million in 2017, only four surpassed $400 million 5 years later.

5. M&A Recalibrated: In the short term, beauty mergers-and-acquisitions activity may not deliver as many megadeals as seen across the industry in the past, but the deal making will continue to be buoyant

- Beauty brands’ average EBITDA margins are around 15-25%, making them attractive to deal-makers.

“The State of Fashion: Beauty,” a new report from The Business of Fashion and McKinsey & Company, is released ahead of The Business of Beauty Global Forum 2023. Read the full report.